Contact Center Challenges And Priorities

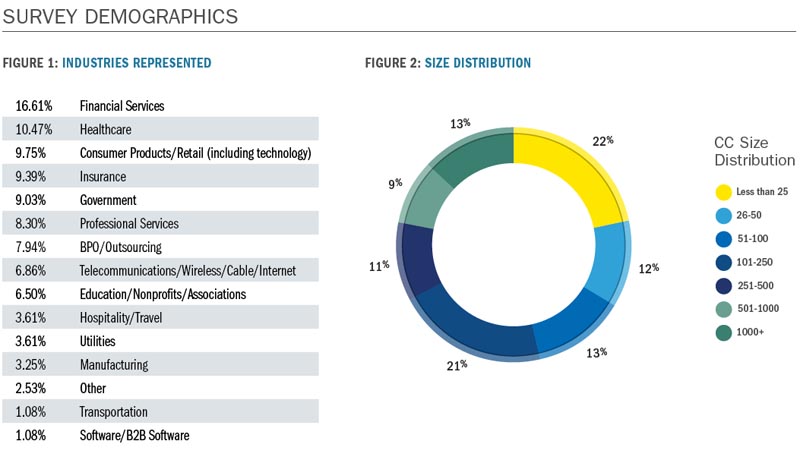

In late 2015, we conducted a simple survey that received input from 277 respondents on two fronts: the biggest challenges today and top priorities for 2016. Participants could identify three of each, with no ranking. Input came primarily from contact center leaders (65%), along with support analysts (10%), IT (8%), supervisors (7%), consultants (4%), and a smattering of others. Figures 1 and 2 show the nice cross section of industries and distribution of sizes we achieved from our contributors—thank you!

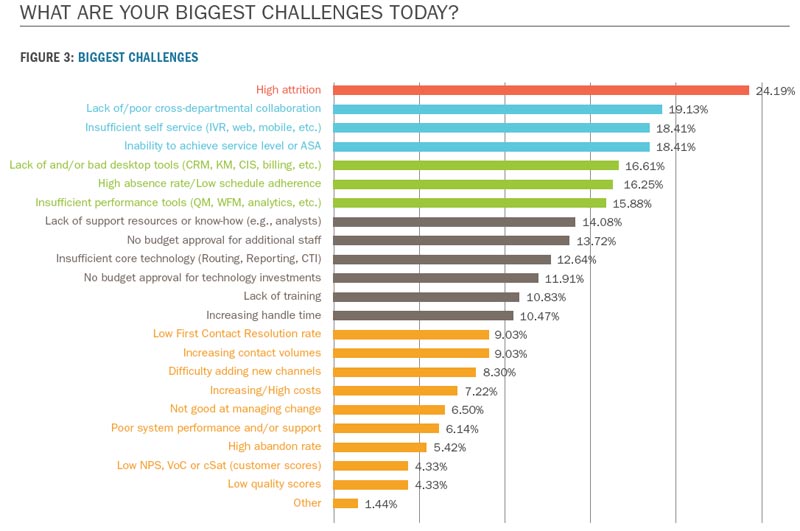

We chose to do this survey because everyone wants to know what challenges people face overall, and within their center size and industry. And, there are so many possible changes to pursue, not to mention the barrage of input from various industry sources, it’s invaluable to learn what priorities are really making it to the top of “to-do” lists. Figures 3 and 4 give you the results.

But let’s not stop at a few charts. We’re going to share our assessment of the results and what they tell us about centers and about our market. We’ll look at trends by industry and by size (Tables 1 and 2), and weave in some commentary on what we think might be behind the results based on our experience.

TOP CONTACT CENTER CHALLENGES

The challenges reveal a diverse top four, shining a light on issues with frontline staff (attrition), leadership (cross-departmental collaboration), technology (self-service), and operational management (Service Level [SL]/Average Speed of Answer [ASA]). No one challenge hits a majority, but attrition is a strong leader, chosen by one in four respondents. (See Figure 3.)

So what’s behind these challenges? Attrition is an age-old problem in contact centers and may be getting worse as the economy improves and the unemployment rate goes down. Organizational silos are all too prevalent and can lead to the departmental collaboration issues and hinder self-service improvement. It’s difficult to achieve a common focus on customer service and sales across most companies. The contact center often has the data to guide improvements but lacks corporate initiatives to ensure that information gets to and engages critical departments. Further, there is often no mechanism to get the project defined and submitted for prioritization, approval and funding.

Meeting SL and ASA depends on many factors across people, process and technology, not to mention adequate budgets. Many challenges noted in the top nine responses point to potential root causes, including budget for staff, performance tools and analysts, and of course attrition and attendance. Poor desktop tools are something we see frequently and know it can be really tough to solve, especially since it generally requires crossdepartmental collaboration. While elevated handle time and low First-Contact Resolution (FCR) are often results of poor desktop performance, they aren’t identified as top problems here (each 9%, or selected by less than 1 in 10).

Our survey identified a large middle ground, with many different and varying challenges in the medium-high (10%-20% of respondents) range. Budget is in the top half—for staff and technology—but high costs ranked relatively low (1 in 14). Lack of training is right in the middle of the list. Perhaps the bigger issue is quality of training and the time to train and reach proficiency based on what we see in projects. We’ll look at this issue in the priorities as well.

Less than 5% identified quality and customer scores as an issue, even though there is a big focus on “Customer Experience” in the industry and a belief bolstered by independent customer satisfaction studies that customer service is not so good in many cases. Here’s my hypothesis: QM scores are sometimes inflated, leaving leaders passively content, and companies use Net Promoter Score (NPS) or similar metrics to get an overall thumbs up from customers and equate that to satisfaction with the contact center interaction.

Other perceived industry problems to solve, such as “omnichannel” (aka multichannel), increasing costs, poor system performance and managing change were not frequently selected issues. Industry hype does not always align with what happens in the trenches. Perhaps many think they are basically good enough at these things compared to other issues. For example, most centers have many channels and things are working OK, even if not integrated. Many believe “we’re good at change” just because they do it a lot, not necessarily because they have seen great results on project outcomes and the return on investment.

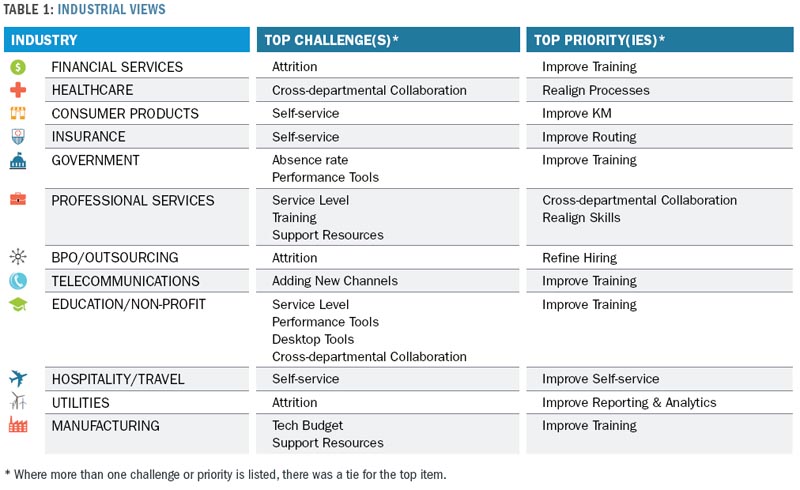

CHALLENGES BY INDUSTRY

As we slice the data by industry, we find the top challenges align with the overall top four (high attrition, self-service, cross- departmental collaboration, SL/ASA). After that, they are all over the map! Attrition is very strong for financial services, BPO, utilities and “other.” Manufacturing seems to struggle with budget for technology as well as lack of support resources and know-how. Insurance points strongly to desktop and self-service, revealing a focus on addressing technology needs. (See Table 1.)

Interestingly, three industries that are very competitive and presumably have to be very customer focused— hospitality/travel, consumer products, insurance—rank self-service challenges high. These industries haven’t made great headway in the past on IVR self-service because of the nature of their interactions and frequency of contact. All that could change with the increasing use of mobile devices. Book a flight/hotel/car, check in, buy some shoes, check for status on three recent orders, file a claim… these are all much easier on a mobile device.

Interestingly, three industries that are very competitive and presumably have to be very customer focused— hospitality/travel, consumer products, insurance—rank self-service challenges high. These industries haven’t made great headway in the past on IVR self-service because of the nature of their interactions and frequency of contact. All that could change with the increasing use of mobile devices. Book a flight/hotel/car, check in, buy some shoes, check for status on three recent orders, file a claim… these are all much easier on a mobile device.

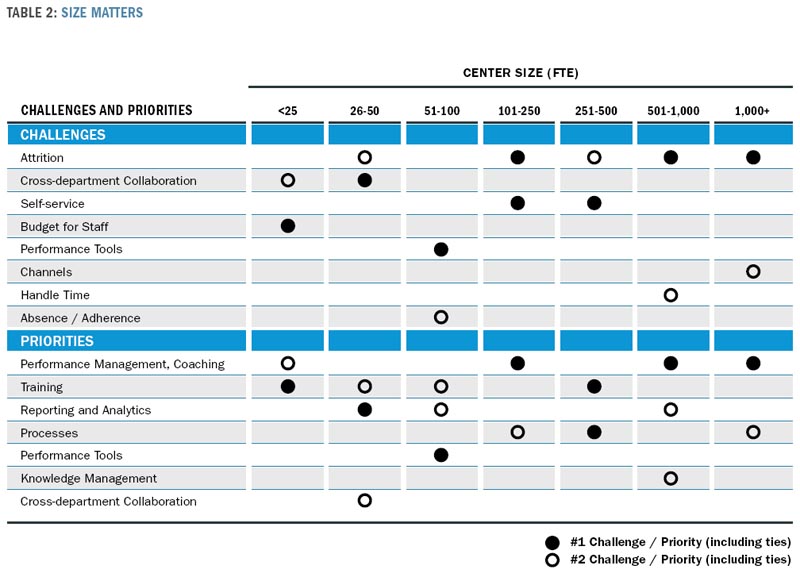

CHALLENGES BY SIZE

Attrition, self-service and cross-departmental collaboration consistently rise to the top across nearly all sizes. Not surprisingly, attrition is most frequently noted for the largest centers (500 and up) and interestingly, it ranks lower (under 10%) for under 25 and 51-100 seats. Self-service is less of an issue for larger organizations. Desktop tool issues were noted at every size. (See Table 2.)

The really large centers (1,000+) are the only size to more frequently mention trouble adding channels and have a very distributed set of issues except for attrition (43% included). Performance (e.g., SL/ASA, FCR) and technology are the least of their worries. Small centers (1-25) struggle to get budget for staff, and correspondingly struggle to meet SL/ASA. It’s tough to succeed when you are understaffed and lack economies of scale.

The really large centers (1,000+) are the only size to more frequently mention trouble adding channels and have a very distributed set of issues except for attrition (43% included). Performance (e.g., SL/ASA, FCR) and technology are the least of their worries. Small centers (1-25) struggle to get budget for staff, and correspondingly struggle to meet SL/ASA. It’s tough to succeed when you are understaffed and lack economies of scale.

Not surprisingly, large centers (1,000+) most frequently note change as an issue. In contrast, small (50 and under) have the biggest issues with cross-departmental collaboration. Stay tuned for how these challenges play out in priorities.

TOP CONTACT CENTER PRIORITIES

The priorities don’t necessary align with the challenges noted (more on that below), but they do align with gaps we see with our clients (see Figure 4). The top need is to improve performance management and coaching. Training is second, focused on the amount, content and/or quality. Given the training challenge ranked relatively low, training prioritization is probably more about the nature of the training and time to proficiency. Similarly, the focus of these priorities on the frontline staff probably aren’t about quality and customer satisfaction; they are about how we address the top issue, attrition. Time to do training right and back it up with consistent and effective coaching. Another top priority emphasizes a key part of the success of those well-trained and coached agents; 23% put improving and automating processes in their top three.

A cluster of things that point to the need for technology improvements follows this focus on people and process. The priorities start with reporting and analytics (over 23%), Knowledge Management (KM), performance tools and self-service, followed by desktop and routing. Of course, we have to throw in the usual caution about technology alone fixing everything; each of these tools have a high people need to accompany them, and they will deliver greater value with the process focus as well.

Many of the top 10 priorities require investment, whether in technology or people. About 1 in 10 want to refine hiring, and the same numbers cited hiring additional staff. Outsourcing is not high on priorities for many (less than 7% noted), perhaps indicating that trend is waning.

Additional media is not on most radars for 2016 (only 1 in 20!). That immediately raises the question of whether this input is contrary to the omnichannel message in the industry. Perhaps the data is conveying centers either have the channels they need, or they have other things to focus on. And it may be this input can peacefully coexist with the omnichannel message and now it’s time to do it better, with greater integration and visibility across channels (more hype—it’s all about the customer experience—whatever channel(s) they use). Remember, someone has to “lead” the overall effort, so this input may reflect the dearth of corporate-level omnichannel initiatives. Further, as many focus on self-service, they will change the channel mix of the environment and alter the omnichannel issues.

PRIORITIES BY INDUSTRY

Performance management/coaching is a frequently cited priority for all verticals except insurance (Table 1). Training is a very strong focus for manufacturing, education/non-profit, financial services, and government, but it not a frequently noted priority for telecom and hospitality/travel. Reporting and Analytics (R&A) is the top priority for many utilities and insurance companies, but cited by less than 1 in 5 for healthcare, consumer products, and education/non-profit. Only 1 in 10 BPOs have R&A in their top three, probably because they have to be good at this (so hopefully already are?!). The other overall priority, process improvement, was fairly low frequency for education/non-profit, insurance, professional services and telecom, only one for government noted it and it is not on the list for hospitality/travel.

KM is big for consumer products, telecom and education/non-profit, and certainly has big potential to have a significant impact in these verticals. Implementing performance tools is fairly high priority for most and goes hand-in-hand with the top priorities noted.

Half of the hospitality/travel participants put selfservice as a priority, with over one-third indicating routing, R&A and performance management. Their different focus perhaps reflects greater change in the customer interfaces and channels in this industry. Insurance deviated a bit from the other verticals, with nearly half indicating changes to routing, including multimedia, are high on their priority list. BPOs are focused on staff development, identifying their top three priorities as hiring, training and performance management.

PRIORITIES BY SIZE

Apparently size sometimes matters—but not always—when it comes to priorities. Relatively large centers (251-500 and 1,000+) are widely distributed in their priorities, while other sizes have a bit more focus. Performance management (one of the most frequently cited priorities at all sizes), training, processes and R&A surface as fairly important across size bands (Table 2). However, improving training is much more important to small centers (42% for smallest, around 30% for 26-50 and 51-100) than for large centers (23% for 501-1000, 11% for 1000+). Process automation/ improvement and R&A were less important to very small centers (only 1 in 6 cited).

In line with the surprising challenge, small centers (50 and under) showed the biggest focus on collaboration with other departments, perhaps because it’s something that can be tackled and/or is extremely important to them. Larger centers (and presumably organizations) could have a greater cynicism about tackling this issue. Very big and very small centers want to increase support resources.

In line with the surprising challenge, small centers (50 and under) showed the biggest focus on collaboration with other departments, perhaps because it’s something that can be tackled and/or is extremely important to them. Larger centers (and presumably organizations) could have a greater cynicism about tackling this issue. Very big and very small centers want to increase support resources.

While outsourcing is not a top priority, it surfaces more for big centers.

ALIGNING CHALLENGES AND PRIORITIES

Figure 5 provides a snapshot view of the alignment—or lack thereof—between challenges and priorities. The top challenge of attrition stands out, and the top priorities of performance management/coaching and training align to help tackle that issue. Beyond that, the big challenges don’t directly align with the top priorities—perhaps because they are difficult and allude to a dependence on others. So centers focus on what they can control and accomplish within their walls, using their own resources. Collaboration is one great example of a big issue with little desire or will to focus on in 2016. Self-service is a bit less complex but still out of the control of most center leadership. These challenges without prioritization point to opportunities down the road that certainly align with industry messages about customer experience and omnichannel success.

As these complex challenges recede, a slew of things that can improve the customer experience and center performance move up the priority list. Reporting and analytics, process improvement, and knowledge management can contribute greatly to SL, ASA, FCR and overall optimization.

As these complex challenges recede, a slew of things that can improve the customer experience and center performance move up the priority list. Reporting and analytics, process improvement, and knowledge management can contribute greatly to SL, ASA, FCR and overall optimization.

2016 will be an exciting year that will hopefully bring improvements for the most valuable resource in the center, frontline staff, and they will in turn leverage tools and support resources to deliver great customer benefit.

We’ll plan to ask the same questions again at the end of 2016 and assess changes and trends. We hope you’ll participate and tune in!

We’ll plan to ask the same questions again at the end of 2016 and assess changes and trends. We hope you’ll participate and tune in!

Lori Bocklund is Founder and President of Strategic Contact.

– Reprinted with permission from Contact Center Pipeline, http://www.contactcenterpipeline.com